The Path to Four Billion: Is Global Crypto Adoption Entering a Hyper-Growth Phase?

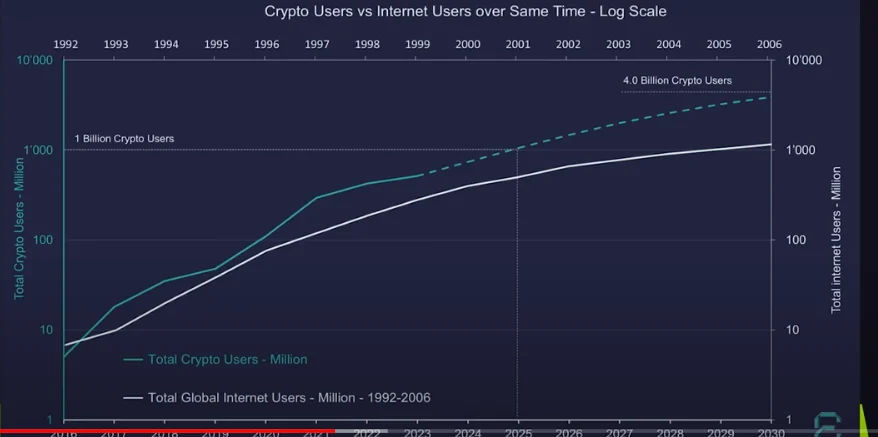

In the fast-evolving landscape of digital finance, few voices carry as much weight as Raoul Pal. The former Goldman Sachs executive and current CEO of Real Vision recently unveiled a provocative, data-driven analysis suggesting that the global adoption of Bitcoin and broader cryptocurrency markets is not merely growing—it is accelerating at a velocity that mirrors, and potentially eclipses, the rise of the early internet. According to Pal’s latest modeling, the world is on a trajectory to see four billion cryptocurrency users by the year 2030, a figure that would represent approximately half of the global population.

The Core Thesis: Crypto’s Aggressive Adoption Curve

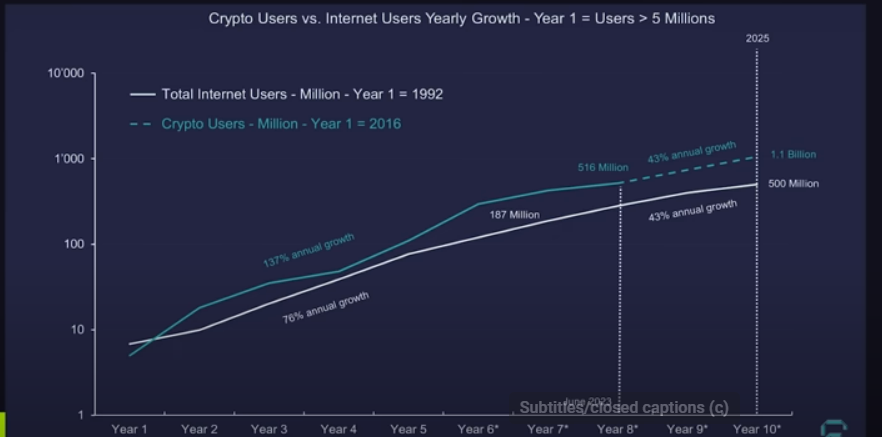

The foundation of Pal’s argument rests on a comparative analysis between the historical growth of the internet and the current user acquisition rates of the cryptocurrency ecosystem. By mapping crypto’s growth trajectory since 2016—the year the industry reached its first million users—against the historic adoption curves of the internet in the 1990s, Pal identifies a distinct, aggressive pattern.

While the internet, often cited as the fastest-growing technology in human history, maintained a growth rate of 76% per year during its infancy before tapering to 43% after its eighth year, cryptocurrency has maintained a staggering growth rate of 137% annually. As of the latest data, the crypto ecosystem boasts approximately 516 million users, a figure that dwarfs the 187 million users the internet claimed at a comparable stage of its lifecycle.

Pal’s projection is conservative by design; he assumes that as the market matures, the rate of crypto adoption will eventually decelerate to match the historical pace of the internet. Even under these "slowed" conditions, the model predicts that the industry will breach the one-billion-user milestone by the end of 2025.

A Chronology of Digital Transformation

To understand the scale of this shift, it is essential to view the timeline of digital adoption through a historical lens.

The Early Phase (2016–2020)

The period between 2016 and 2020 served as the "proof-of-concept" era for the industry. During these years, Bitcoin moved from a fringe curiosity for cypherpunks and niche investors to an institutional-grade asset class. The introduction of derivatives, the maturation of exchanges like Coinbase and Binance, and the burgeoning decentralized finance (DeFi) movement catalyzed a transition from speculative hobbyism to early-stage professional infrastructure.

The Acceleration Phase (2021–2023)

The post-pandemic economic environment acted as a massive accelerant. As central banks implemented unprecedented monetary expansion, Bitcoin’s narrative as "digital gold" gained significant traction. This period saw the entry of major institutional players, such as MicroStrategy and Tesla, alongside the mainstreaming of non-fungible tokens (NFTs) and the rapid expansion of Layer-2 scaling solutions. These developments lowered the barriers to entry, making the ecosystem more accessible to the average consumer.

The Current Landscape and Future Outlook (2024–2030)

We are currently in a pivotal transition toward mass-market infrastructure. With the integration of Spot Bitcoin ETFs and the increasing focus on regulatory clarity in jurisdictions like the European Union and the United Arab Emirates, the ecosystem is shifting toward "invisible" adoption. By 2030, Pal suggests that the technology will have moved from a "voluntary" financial choice to an integrated layer of the global digital economy.

Supporting Data: Why Four Billion is Mathematically Plausible

The assertion that four billion people will utilize digital assets within six years may seem hyperbolic at first glance, but the supporting metrics suggest a strong foundation.

- Network Effects: Metcalfe’s Law, which states that the value of a network is proportional to the square of its users, has been a reliable predictor for Bitcoin’s price and adoption. As the number of active wallet addresses increases, the utility of the network grows exponentially, creating a "flywheel effect" that attracts further users.

- Mobile Penetration: Unlike the early internet, which required access to expensive desktop computers, the modern crypto ecosystem is primarily mobile-first. With billions of people globally already owning smartphones, the distribution infrastructure for crypto wallets is already in place.

- Financial Inclusion in Emerging Markets: Much of the projected growth is expected to come from the Global South. In regions with unstable fiat currencies and limited access to traditional banking, Bitcoin and stablecoins offer a lifeline. For these populations, crypto is not a speculative investment but a necessary tool for survival, remittances, and store of value.

Expert Analysis and Official Perspectives

While Raoul Pal’s projections are widely followed, they exist within a broader debate among economists and technology analysts.

Institutional skeptics often point to the "volatility problem" and the lack of consumer protections as barriers to mass adoption. Critics argue that until digital assets are more stable and the user experience is "idiot-proof"—where a user doesn’t need to understand private keys or blockchain protocols—adoption will plateau.

Conversely, proponents of the "institutionalization" narrative point to the massive shift in how traditional finance views digital assets. Figures from BlackRock, Fidelity, and other asset managers have signaled that the integration of digital assets into retirement portfolios and corporate balance sheets is a matter of "when," not "if." This institutional mandate provides the legitimacy required to onboard the next several billion users who may not be "crypto-native" but trust their legacy financial providers.

The Socio-Economic Implications of Mass Adoption

Should the world hit the four-billion-user mark by 2030, the implications for the global financial order would be profound.

Decentralization of Monetary Policy

Mass adoption would fundamentally weaken the ability of sovereign nations to use monetary policy as a blunt instrument. If a significant percentage of the global population opts for a decentralized, deflationary asset, the traditional model of inflationary fiat printing becomes increasingly difficult to sustain without inducing capital flight into digital assets.

The Death of the "Unbanked"

The most profound humanitarian impact would be the elimination of the "unbanked" status for millions of people. A digital wallet on a smartphone provides an individual with a global bank account, allowing them to transact internationally, save in a currency that is not subject to local hyperinflation, and access credit markets that were previously closed to them.

Evolution of the Internet (Web3)

Finally, this level of adoption implies a total shift in the architecture of the internet. Web3, or the "value-layer" of the internet, would become the default standard. Ownership of data, identity, and digital assets would be native to the browsing experience, fundamentally shifting the power dynamic from centralized tech giants to the individual users.

Conclusion: A Paradigm Shift in Progress

Raoul Pal’s analysis provides a sobering and exhilarating look at the potential future of digital assets. Whether the industry hits exactly four billion users by 2030 is secondary to the undeniable trend: the digitization of value is accelerating at a pace that is fundamentally altering the way the world views money, ownership, and financial freedom.

While volatility remains a hallmark of the asset class, the long-term adoption curve suggests that we are witnessing the migration of the global economy onto blockchain rails. For investors and observers alike, the coming years will not just be about price action, but about the transition from a niche technological experiment to the new infrastructure of human civilization.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency investments involve significant risk of loss. Always conduct your own thorough due diligence and consult with a certified financial advisor before making any investment decisions.