The Great Capitulation: Why Bitcoin Miners Are Offloading Reserves in a Challenging 2026

The Bitcoin mining industry, once defined by its "HODL" ethos and long-term accumulation strategies, is currently navigating its most precarious period in recent memory. As of April 2026, the sector is grappling with a stark reality: approximately 20% of the entire industry is operating at a net loss. This fiscal fragility has forced a seismic shift in behavior among publicly traded mining giants, who are now liquidating their digital assets at record-breaking speeds simply to cover operational overhead and energy costs.

The Economic Squeeze: Profits Eroded by Market Headwinds

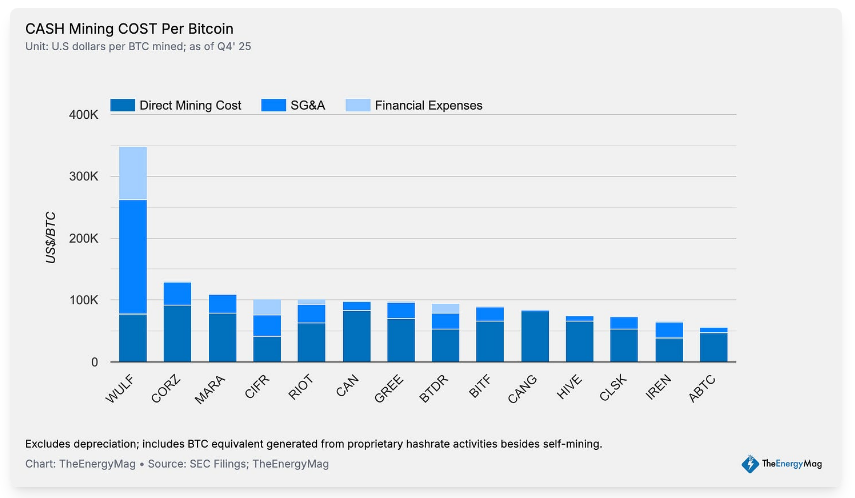

The primary catalyst for this trend is the steady decline of "hashprice"—the industry-standard metric for daily revenue earned per petahash of computing power. Since July 2025, this figure has been in a sustained downward spiral, recently hovering around $33 per petahash per second.

When analyzed against the industry’s breakeven point, which sits stubbornly near $35, the math becomes grim. For miners utilizing older-generation hardware, the gap between operational cost and revenue is not merely a theoretical concern; it is a direct line to insolvency. This margin compression has turned the first quarter of 2026 into a period of institutional distress, with companies like MARA, CleanSpark, Riot, Cango, Core Scientific, and Bitdeer leading a massive, industry-wide sell-off.

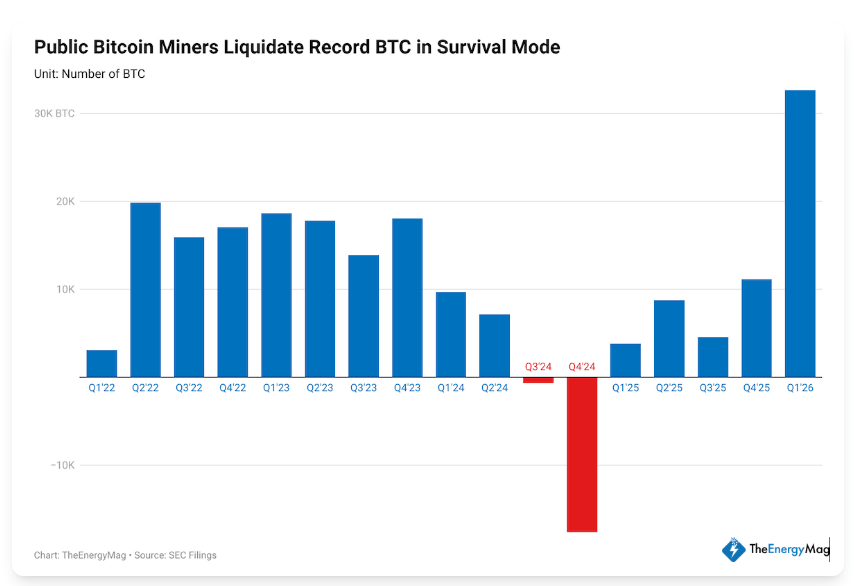

According to data compiled by TheEnergyMag, these major players collectively offloaded over 32,000 BTC in the first three months of the year. To put this in perspective, this single-quarter figure exceeds the total volume sold by these companies across the entire 2025 calendar year. Furthermore, it shatters the previous quarterly record of 20,000 BTC, which was set during the tumultuous Q2 2022 market collapse following the implosion of the Terra-Luna ecosystem.

A Chronology of Declining Reserves

The current wave of selling is not a sudden reaction to a single market event, but rather the culmination of a multi-year trend. CryptoQuant’s tracking of miner reserves indicates a consistent depletion of Bitcoin holdings that began as early as 2023.

At the end of 2023, the global mining community collectively held roughly 1.86 million BTC. By April 2026, that figure has drifted downward to approximately 1.8 million. While this decline has been gradual, the aggressive liquidations observed in Q1 2026 suggest an acceleration of this trend.

The timeline of this pressure can be traced through three distinct phases:

- The Post-Halving Reality (Mid-2025): The immediate aftermath of the most recent halving event significantly reduced block rewards, effectively doubling the difficulty of maintaining profitability.

- The Hashrate Escalation (Late 2025): The global network hashrate reached new peaks throughout the latter half of 2025. While this demonstrates the network’s security, it created an "arms race" dynamic, forcing miners to invest in more efficient equipment while simultaneously competing for a smaller pool of daily rewards.

- The Q1 2026 Liquidation Wave: Facing mounting energy bills and high interest rates on debt used to finance hardware expansions, miners reached a breaking point, resulting in the record-shattering sell-off reported in early April.

Supporting Data: Why the Breakeven Point Matters

The mining business model is fundamentally a commodity-based enterprise. Unlike traditional tech companies, miners have little control over the price of the asset they produce, yet they face high, fixed operational costs—primarily electricity.

When the price of Bitcoin remains stagnant or under downward pressure, and the cost to produce a single Bitcoin (the "production cost") rises due to network difficulty and electricity pricing, the only variable left to adjust is the treasury. Analysts from CoinShares, in their Q1 2026 Bitcoin Mining Report, highlighted that this is a classic "capitulation" phase. They warn that unless the market price of Bitcoin experiences a meaningful, sustained rally, the industry should brace for further consolidation.

Higher-cost operators—those without access to low-cost power purchase agreements (PPAs) or those running older, less efficient ASIC machines—are the most vulnerable. For these firms, the "selling to pay the lights" strategy is not a long-term plan; it is a survival tactic that, if prolonged, risks the total exhaustion of their Bitcoin treasuries.

The Counter-Trend: Corporate Treasuries and Institutional Accumulation

While the mining sector has been forced into a defensive posture, a distinct counter-movement is occurring at the corporate treasury level. The liquidity provided by miners offloading their BTC is being absorbed by a different class of investor: the "Corporate HODLer."

Strategy, the largest corporate holder of Bitcoin, continues to signal its unwavering commitment to the asset. Following a pattern that has become synonymous with institutional confidence, co-founder Michael Saylor recently took to social media to hint at further acquisitions. By sharing the company’s BTC acquisition history chart, Saylor signaled to the market that the current price dip is viewed as an opportunity rather than a deterrent.

This dynamic creates a fascinating divergence in the Bitcoin ecosystem: the producers (miners) are being forced to sell to survive, while the allocators (treasury buyers) are utilizing the increased market supply to further consolidate their positions. This shift suggests that Bitcoin is moving from a distributed mining-held asset toward a concentrated institutional asset.

Implications for the Future of Mining

The implications of this current crisis are twofold. First, the sector is likely headed for a period of intense M&A (Mergers and Acquisitions) activity. Smaller, inefficient mining operations that cannot sustain the current hashprice will likely be acquired by larger, better-capitalized firms with superior access to energy infrastructure. This will lead to a more centralized, but perhaps more resilient, mining industry.

Second, the relationship between miners and the price of Bitcoin is entering a new phase. In the past, miners were considered long-term "price supporters" who rarely sold unless necessary. Now, their role as potential "forced sellers" adds a layer of selling pressure during market downturns. As long as the hashprice remains below the $35 threshold for a significant portion of the network, the market must account for the fact that miners will continue to introduce supply into the market to meet their operational expenses.

Ultimately, the Q1 2026 period serves as a stress test for the Bitcoin mining industry. It is a transition from an era of unchecked expansion to one of efficiency and fiscal discipline. As the weaker players capitulate, the survivors will be those who can optimize their energy consumption, secure long-term capital, and weather the volatility of a market that, while rewarding for holders, remains unforgiving to producers.

As the industry looks toward the remainder of 2026, the key question remains: will the market price of Bitcoin rise to meet the miners’ production costs, or will the miners be forced to innovate their way out of a cycle that has pushed them to the brink? For now, the charts suggest that the era of easy mining profitability is over, replaced by a ruthless environment that prioritizes those with the deepest pockets and the most efficient operations.