The Quiet Revolution: Citigroup Predicts Blockchain’s Trillion-Dollar Inflection Point

In the landscape of modern finance, few institutions carry the weight of Citigroup. As one of the world’s most influential banking giants, its strategic outlook often serves as a barometer for institutional sentiment toward emerging technologies. A comprehensive new report from the firm, titled "Money, Tokens, and Games: Blockchain’s Next Billion Users and Trillions in Value," suggests that we are currently standing on the precipice of a massive, industry-defining shift.

While blockchain technology has weathered significant market volatility and regulatory scrutiny, Citigroup analysts posit that the underlying infrastructure is poised for hyper-growth. According to the bank, the era of "invisible" blockchain adoption—where the technology functions seamlessly in the background of everyday applications—is rapidly approaching, promising to unlock trillions of dollars in value by 2030.

Main Facts: The Transition from Infrastructure to Utility

The core argument presented by Citigroup is that blockchain has suffered from a "visibility problem." Unlike the internet, which gave rise to intuitive browsers and social media platforms, or the automobile, which revolutionized personal mobility, blockchain has remained largely a back-end infrastructure layer.

The Complexity Barrier

Citigroup notes that the technical barriers to entry and the lack of a user-friendly "front-end" have hindered the widespread adoption of decentralized ledgers. For the average consumer, interacting with a blockchain often involves managing private keys, navigating complex wallets, and understanding decentralized finance (DeFi) protocols.

However, the report argues that this friction is temporary. The next generation of blockchain innovation will move away from complex, niche applications and toward integrated, consumer-facing experiences where the user may not even be aware they are utilizing distributed ledger technology (DLT). This transition is viewed as the "inflection point" that will lead to a billion-plus user base.

Chronology: A Path to Mainstream Integration

The journey toward institutional and mass-market blockchain adoption has been a gradual, often tumultuous process. Understanding the trajectory helps contextualize Citigroup’s optimistic 2030 outlook.

- 2009–2015: The Experimental Phase. Blockchain begins as a fringe technological experiment with the launch of Bitcoin, primarily attracting developers, cypherpunks, and early speculative investors.

- 2016–2020: The DeFi and Smart Contract Explosion. The rise of Ethereum introduces smart contracts, allowing developers to build decentralized applications (dApps). This period sees the birth of DeFi, stablecoins, and the initial institutional interest in enterprise blockchain.

- 2021–2022: The Hype Cycle and Market Realignment. A period of intense speculation, the proliferation of NFTs, and the subsequent "crypto winter." This phase forced the industry to shift focus from speculative asset pricing to sustainable infrastructure and real-world utility.

- 2023–2025: The Infrastructure Maturation Phase. Increased regulatory clarity in major jurisdictions (such as the EU’s MiCA regulation) and the emergence of institutional-grade custody solutions.

- 2026–2030: The Adoption Inflection. Citigroup predicts this period will see the mass rollout of CBDCs, the tokenization of global private markets, and the integration of blockchain into mainstream gaming and social media platforms.

Supporting Data: By the Numbers

Citigroup’s report is not merely speculative; it is grounded in aggressive economic modeling. The bank highlights three primary engines of growth: Central Bank Digital Currencies (CBDCs), real-world asset (RWA) tokenization, and consumer-facing Web3 applications.

1. The CBDC Explosion

By 2030, Citigroup estimates that up to $5 trillion worth of CBDCs could be in circulation across major global economies. Crucially, the bank anticipates that nearly 50% of this total could be linked to DLT, providing a massive, state-sanctioned liquidity pool that integrates blockchain into the bedrock of global monetary policy.

2. The Tokenization of Real-World Assets (RWA)

Perhaps the most significant finding in the report is the prediction regarding tokenization. Citigroup forecasts an 80x growth in the tokenization of financial and real-world assets. By 2030, this sector is expected to reach an estimated $4 trillion in total value. This represents a seismic shift for private markets, enabling fractional ownership, increased liquidity, and automated compliance through smart contracts.

3. The "Invisible" User Base

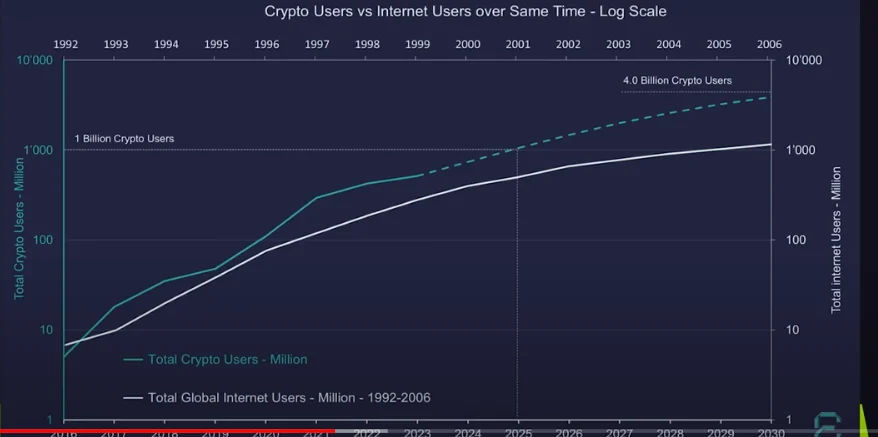

The report emphasizes that true mass adoption occurs when the technology becomes invisible. Whether it is through social media platforms integrating micropayments or gaming ecosystems utilizing non-fungible tokens (NFTs) to manage in-game assets, the goal is to reach a billion users who are benefiting from the efficiency of the blockchain without needing to interact with the underlying technical complexity.

Official Perspectives: Banking on the Future

Citigroup’s stance represents a broader trend of "cautious optimism" among major global financial institutions. While banks have historically been skeptical of decentralized assets, the narrative has shifted toward integrating blockchain as an efficiency tool.

In the report, Citi analysts remark:

"Successful adoption will be when blockchain has a billion-plus users who do not even realize they are using the technology. This is likely to be driven by the adoption of central bank digital currencies (CBDCs) by large central banks as well as tokenized assets in gaming and blockchain-based payments on social media."

This perspective highlights a departure from the "crypto vs. banks" narrative. Instead, the focus has shifted toward "bank-friendly" blockchain implementations—such as permissioned ledgers and regulated tokenized assets—which allow traditional finance (TradFi) to maintain control while leveraging the speed and transparency of DLT.

Implications: A New Financial Paradigm

The implications of Citigroup’s findings are profound, touching on everything from global trade to the nature of personal property.

Impact on Global Finance

The shift toward tokenized assets could fundamentally alter the cost of capital. By removing intermediaries in clearing and settlement processes, blockchain can significantly reduce transaction costs. For institutional investors, this means the ability to move assets across borders in near real-time, 24/7, without the bottlenecks of legacy banking hours or correspondent banking networks.

Impact on the Consumer

For the average user, the integration of blockchain into social media and gaming implies a world where digital ownership is verified and transferable. The ability to own a digital asset—whether a skin in a game or a social media handle—without relying on a centralized corporate entity creates a new digital economy. When combined with the speed of CBDC payments, the result is a seamless financial experience that could render current payment rails obsolete.

Regulatory Challenges

Despite the optimistic outlook, the transition is not without hurdles. Citigroup acknowledges that the path to 2030 will be defined by how central banks and governments navigate the regulatory landscape. Issues surrounding anti-money laundering (AML), privacy, and the interoperability of different DLT systems remain significant obstacles that must be overcome to achieve the scale predicted by the bank.

Conclusion: The Long View

Citigroup’s report serves as a reminder that while the blockchain industry often focuses on daily price movements and short-term volatility, the long-term arc of the technology remains focused on infrastructure modernization. By projecting that trillions of dollars in value will migrate onto distributed ledgers, the banking giant is signaling that blockchain has moved past its "proof of concept" phase.

As we look toward 2030, the winners of this transition will likely be those who successfully bridge the gap between complex cryptographic infrastructure and user-centric applications. Whether the prediction of 80x growth in tokenization comes to fruition or not, the message from one of the world’s largest banks is clear: the blockchain is no longer a peripheral experiment—it is the next phase of the global financial engine.

Disclaimer: The information presented in this report is for educational and informational purposes only and does not constitute financial, investment, or legal advice. Investing in digital assets, including cryptocurrencies and tokenized securities, carries significant risk. Readers are encouraged to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.